Damages For Breach Of Contract: What Can You Claim?

You’ve entered a contract, and the other party hasn’t fully delivered on their promises. Maybe their products or service quality were unsatisfactory. Maybe they were repeatedly late in fulfilling their duties. Maybe their contractual failures even caused you to suffer financial losses. Whatever the case, you are legally entitled to claim damages for such breaches of contract. Here’s a breakdown of when you can claim for damages, and how much you can claim.

What is a breach of contract?

Let’s first understand what constitutes a breach of contract. A breach of contract occurs when one party, without valid justification, fails to live up to their contractual obligations.

Here are some breach of contract examples:

A party fails to perform their duties in the contract

A party fails to fulfill the overall objective of their contract

A party is late in fulfilling their promise in the contract

A party prevents someone else from performing their duty in the contract

A party does something they promised not to do in the contract

Is there a time limit to claim damages for breach of contract?

Yes. Generally, under Section 6 of the Limitation Act, you must sue someone for breach of contract within 6 years of the date of breach.

How do courts go about calculating damages for breach of contract?

No. The court will only award compensatory damages. This means the amount you can claim is limited to restoring you to the position you would have been in if not for the contract breach. The court will not award punitive damages to punish the other party for breaching the contract.

Important: If you have a “penalty clause” in your contract, make sure that the damages specified are a genuine estimate of the loss you would suffer if the contract were to be breached. If the court finds that the penalty is designed to punish the other party (over and above compensating you), the court may invalidate your penalty clause.

What types of damages can you claim for breach of contract?

There are four types of damages you can claim for breach of contract.

#1. Contract damages: These are the damages you would have suffered if the contract had not been breached. This can include the amount stated in the contract, plus consequential damages if you suffer financial losses stemming from the breach.

#2. Liquidated damages: These are damages that are specifically laid out in the contact to compensate parties for breaches. Remember – the courts will only award compensatory damages. Make sure the terms of your contracts – especially any “penalty clauses” – are drafted reasonably. If you’re aiming to punish the other party for breaking the contract, you won’t succeed in front of a judge!

#3. Specific performance: Instead of monetary damages, you can ask the court to order the party in breach to perform their contractual obligations. This occurs when paying damages alone would not adequately compensate the plaintiff. For instance, if the contract involved delivering unique property, like a plot of prime land, damages would likely not sufficiently compensate you.

#4. Injunction: Sometimes, contracts specify for the other party not to do certain things. If the other party fails to live up to such obligations, you can ask the court to serve an injunction on the other party. The court will order the other party not to perform the actions stated in the contract. This is the opposite of specific performance.

How do you go about claiming damages for breach of contract?

There are four methods you can use to claim compensation for breach of contract.

#1. Small Claims Tribunal: If your claim is under $20,000 (or $30,000 with both parties’ agreement), you can file your case with the Small Claims Tribunal. You can’t split your claim into smaller parts to bring it under Tribunal jurisdiction. Both parties cannot be represented by lawyers. You must file your suit within 2 years of the contract breach to file suit with the Tribunal.

#2. Civil litigation: Lawyer up and sue their pants off. Prepare your war chest – legal fees can easily reach hundreds of thousands of dollars, with cases often stretching for years.

Note that court proceedings are open to the public, so if privacy is a concern then arbitration or mediation will be better choices.

#3. Arbitration: If you don’t relish the idea of a long-drawn court battle, you can choose to arbitrate the matter. Both parties will appoint 1-3 independent arbitrators to facilitate a middle-ground resolution to the contract breach. Note that the decision of an arbitration panel is legally binding. If you don’t like the outcome, you can’t abandon the arbitrator(s)’ decision and then file a civil suit. You have to live with the decision.

Arbitration is not necessarily much cheaper than civil litigation; total legal expenses can also easily reach several hundred thousand dollars. However, arbitration is quicker than civil suits, so you won’t have to spend as much time and effort trying to get compensation for the contract breach. There is also the advantage of privacy – arbitration proceedings must legally be kept confidential.

#4. Mediation: If you claim is more than $20,000 but less than $500,000, you should consider mediation.

You can approach the Singapore Mediation Centre to facilitate private mediation between you and the other party. Mediation is significantly less costly than lawsuits or arbitration proceedings. Settlements are also much quicker – disputes can typically be resolved in weeks, rather than years as with lawsuits. Mediation is also a strictly confidential process.

However, mediation is not legally binding. If the other party fails to live up to the agreed settlement, you’ll either have to commence more mediation, or bring them to court.

#5. Ministry of Manpower: If the breach of contract was between an employer and employee, then as a worker you can approach the Ministry to resolve the dispute. This applies to any worker covered by the Employment Act. The only workers not covered by the Act are:

Seafaring workers

Domestic workers

Civil servants

Ready to protect your business?

Provide helps small businesses get tailored coverage at better prices. You’ll save up to 25% on your premiums. Our online operating model creates lower overheads, so we pass every dollar saved back to you.

Delighting large numbers of people with food can be a really rewarding profession. However, it’s also a business that’s fraught with significant liability and operational risks. If you run a catering business, it’s important to understand what could go wrong, so you can take active steps to prevent them from happening to you.

We break down the 5 worst risks for caterers, and how business owners can protect themselves from them.

#1. Foodborne illnesses

This is probably the biggest liability risk that catering businesses face. Food that isn’t cooked and stored properly may become contaminated with dangerous bacteria, causing sickness or even death in people you serve it to. Employees may forget to wash their hands, or allow raw food to come into contact with cooked food. It only takes one minor mistake to contaminate an entire batch of food – using a knife for raw meat to cut salads, forgetting to clean a kitchen table, leaving cooked food uncovered for long periods of time, forgetting to wash your hands after using the restroom, etc. So many things can easily go wrong and cause cross-contamination in catering kitchens.

Singaporean caterer causes mass food poisoning, man dies:

In 2018, a local restaurant called Spize caused a mass food poisoning outbreak after it had catered food for a corporate client. More than 75 people came down with severe gastroenteritis. One man even suffered organ failure and died. Singaporean authorities swiftly investigated the restaurant. The NEA (National Environment Agency) discovered severe hygiene lapses that caused a widespread salmonella outbreak in both Spize’s food and kitchen facilities. NEA uncovered faecal matter in the bento sets Spize had catered. Salmonella and other bacteria were also discovered throughout Spize’s kitchen: on door handles, fridge handles, and multiple work surfaces. There was no soap in Spize’s employee toilets, which likely contributed to faecal matter passing from workers to the food they were preparing. Workers had also freely mixed cutting boards and knives for raw meat with uncooked food, causing cross-contamination.

#2. Food spoilage

Catering businesses usually have to maintain large inventories of food to meet customer demand. However, having such big stockpiles of produce creates serious risks of food spoilage if something goes wrong. If the fridges and freezers break down, coolant leaks occur, the power trips for extended periods, or other mechanical failures occur, then all this produce would rapidly spoil in our tropical heat.

Spoiled produce isn’t just a health hazard, it’s massively costly to your catering business

Spoiled produce creates two big adverse impacts to caterers:

Food poisoning liability: As in point #1, food that isn’t properly refrigerated can quickly become contaminated with dangerous bacteria. Customers who fall sick from consuming your food can hold you liable for medical expenses, and demand legal damages.

Inventory replacement cost: Spoiled stocks need to be replace.

Many catering businesses operate on slim margins. Labour costs and ingredient prices are high and rising. Having to replace a big amount of spoiled stock can cause a significant cash flow crunch. It’s important to have a Business Package Insurance policy, which will cover replacement costs if your produce or cooked food spoils due to storage equipment breakdowns.

#3. Machinery damage & breakdown

If you operate a central kitchen, you’ll need coverage to protect your expensive kitchen equipment from damage and breakdowns. You’ll want to protect costly industrial equipment like stoves, ovens, hoods, from mechanical failures, power surges, and other damage that could harm your ability to produce food for customers.

Machinery damage or breakdowns levy two significant costs on caterers:

Repair/replacement cost: Broken machines have to be fixed or replaced entirely.

Lost income: Broken machines can’t produce food. You might lose some sales if you can’t deliver sufficient quantities of food.

All this pretty kitchen equipment is expensive

The great thing about Business Package Insurance is that it covers machinery damage and breakdowns (from selected insurers). This means damage to your machines (e.g. from fire or water leaks) will be covered. Business Package Insurance also covers lost income from machine damage/breakdowns, so you’ll get a daily cash payout for each day that you can’t operate your business because of broken kitchen equipment.

#4. Worker accidents

Injuries are common with catering workers, creating liabilities for business owners

With so many food workers operating in a fast-paced environment filled with hot items and sharp tools, it’s inevitable that accidents will occur. Under the Work Injury Compensation Act (WICA), businesses are legally liable to pay for injured workers’ medical expenses and lost wages.

It is a legal requirement to have Work Injury Compensation Insurance for:

Manual workers, regardless of salary

Workers earning less than $1,600/month (salary limit will be raised to $2,100 from 1st April 2020)

Here are some amounts your catering business would have to pay for different worker injuries:

Worker job scope: Kitchen assistant

Injury: Severed thumb (injured while cutting food ingredients)

What your business must pay for

Amount

Lump sum compensation for permanent incapacity

$104,040

Medical expenses

$10,000

Lost wages (2 weeks MC)

$1,000

Total:

$115,040

It really is a remarkably staggering cost, isn’t it? More than $100,000 if your worker loses a single thumb – a frighteningly common occurrence especially when you spend 8-12 hours a day chopping stuff non-stop.

Catering staff that commonly need Work Injury Compensation Insurance are: chefs, cooks, kitchen supervisors, kitchen assistants, dishwashers, cleaners, and delivery drivers. It’s also advisable to have Work Injury Compensation Insurance for sales staff, who may get into car accidents if they travel frequently to meet clients.

#5. Business property damage

Fire, explosions, and water leak damage are very real risks that caterers face. A worker could leave the stove on and cause a fire that burns down your kitchen. A malfunctioning oven could explode. Water pipes could leak, damaging your equipment and causing expensive repair costs.

#2. Work Injury Compensation Insurance: This protects you against legal liability for worker injuries. It pays for medical expenses, and legal expenses if you get sued for work-related injuries.

With Provide, you’ll save up to 25% on your insurance premiums. Our online operating model creates lower overheads, so we pass every dollar saved back to you. At Provide, we take pride in understanding the unique risks that each industry and business faces, so we can recommend the best solutions to protect you from such risks.

Non-profits do a great service to the community, but this service is fraught with risks. Hackers could steal highly sensitive data from you. Injuries could strike your staff and volunteers. And worse still, you might inadvertently hurt the people you’re serving if you’re not careful. All these situations create tremendous legal liability and operational disruptions. It’s crucial for non-profits to take steps to mitigate these risks, so that they can fulfil their organisational mission to the best of their ability.

Here’s a list of the 3 biggest risks for non-profits while serving the community:

#1. Data breaches

Imagine telling all your donors, staff, and volunteers that you’ve just been the victim of a data breach.

How bad would their reactions be? How much faith would you lose from your donors? How would it affect staff and volunteer morale? Do you think people would ever trust your organisation as much as the used to?

Getting hacked is a very real threat to non-profits – hackers are increasingly targeting charitable organisations because they’re seen as “soft targets”. If you accept donations online, your organisation will be an even bigger target for hackers looking to steal sensitive information like credit card details or bank account numbers.

The unfortunate reality is that many non-profits are indeed very vulnerable to such attacks because they don’t have robust cyber protection. It’s important for non-profits to have a strong cyber security plan in place. It’s also crucial for non-profits to have cyber insurance to shield themselves against legal liability if they get hacked. Non-profits will face significant legal repercussions if the personal information of their donors, beneficiaries, or volunteers get stolen or leaked all over the internet.

With Singapore’s PDPA law (Personal Data Protection Act), there is also a strong regulatory imperative for securing your data. In 2019, the largest fine for breaching the PDPA was levied on a company called Learnaholic, which was fined $60,000 for data breaches. Non-profits must seriously guard their data.

#2. Professional Liability

Organisation Liability

Unfortunately, just because you’re doing good doesn’t mean you’re absolved from legal liability (if only the world were that kind). Non-profits have a legal obligation to ensure that your services don’t cause harm to anyone. If your services end up injuring people, or causing illness, that you’ll be just as liable as a for-profit corporation in the eyes of the law.

Example Situations:

If you deliver cooked meals, the people who eat your food might fall sick. If the food was contaminated, they may even end up hospitalised. You can be held legally liable for making them ill.

If you run a home or a hospice, you can be held liable for injuries or illnesses that occur to your residents. If a resident falls and injures themselves because there was a puddle on the floor, you can be found negligent and held liable. If a resident falls sick, or has a worsening illness due to your staff providing insufficient care, you ca be found negligent and legally liable.

Directors Liability

Beyond organisational liability, directors of non-profits also face personal liability risks. If your non-profit gets sued, chances are the directors will also get sued personally as well. If you’re a non-profit director and you get sued, your personal assets like your house and savings will be exposed to claims.

Example situation:

You run a non-profit counselling centre for people with mental health issues. One of your counsellors befriends a client outside of work. The counsellor makes inappropriate romantic advances towards the client. The client suffers psychological trauma, and decides to file a lawsuit against your organisation’s directors for not having proper governance structures in place that would have prevented the counsellor’s inappropriate behaviour.

#3. Employee/Volunteer Injuries

Your employees or volunteers may get injured while carrying out work. Non-profits will have often members travelling around the country, or even going overseas, to perform duties. Car accidents could injure your members while they’re on the road. Your members’ duties might involve manual labour like building shelters or lifting heavy items. Accidents can easily occur while doing such physical work. If your members are volunteering in a developing nation, they’re at even great risk of accidents, or falling sick due to diseases contracted there. Many injuries or illnesses could occur during all this travel and work, creating significant legal liabilities for your organisation.

Examples Situations:

Your staff are out delivering food to low-income households. A staff member slips and falls during a delivery, breaking her arm. Under the Work Injury Compensation Act (WICA), your organisation would be liable to pay for her medical expenses and lost wages.

You organise an overseas mission trip to Cambodia to build homes for villagers. While there, some of your volunteers get injured when a roof collapses on them. Some other volunteers contract parasites from dirty water and fall very sick. Your non-profit would be liable for their medical expenses, and could potentially have to pay damages for not sufficiently ensuring your volunteers’ safety.

Under WICA regulations, if you had 4 staff members who died while working, your non-profit would have to pay up to $1 million in compensation ($225,000 * 4) to the families of the deceased.

You might have heard of the terms libel, slander, and defamation. What are the legal differences between these terms? Defamation is actually an umbrella category for statements that harm the reputation of another person or entity. Libel and slander are subcategories of defamation: libel refers to permanent (written or broadcast) defamation, while slander is temporal (spoken) defamation. In this article, we’ll break down 2 of the biggest legal differences of libel vs slander, and how this impacts companies.

Libel

Slander

Communication method

Permanent – written or broadcast

Temporal – spoken

Examples of communication mediums

Newspapers, articles, blog posts, social media posts, videos, radio broadcasts, TV shows

In-person communication, talks, comments at meetings

Need to prove special damages?

No

Yes, with exceptions

Difference #1. Libel is permanent, slander is temporal

You might have read before that libel is written, while slander is spoken. That’s technically incorrect. Libel covers any defamation that’s permanent, whether it’s written or spoken. Under Section 3 of Singapore’s Defamation Act, the “broadcasting of words by means of telecommunication shall be treated as publication in permanent form.” So, if someone makes a video or radio podcast and says insulting words about you, that’s actually libel, not slander.

Slander is temporal defamation that’s spoken. So this would cover rumours that are spread by word-of-mouth, insulting comments made in meetings, or verbal attacks in speeches.

The origins of separating libel from slander hail from the US and UK, which operate on common law systems just as we do. In the US, a landmark defamation was Hartman v. Winchell in 1947, which established that defamatory radio broadcasts constituted libel and not slander. Another landmark “libel vs slander” case was Shor v. Bilingsley in 1956, which ruled that defamatory remarks in a television broadcast were libelous, not slanderous.

This distinction between libel vs slander is important, because the type of evidence you’ll need to produce in a lawsuit alleging libel is different from one alleging slander. This leads us to point 2 below.

Difference #2. Special damages are assumed for libel, but not for slander

Let’s first understand what “special damages” means. Special damages are quantifiable losses that you’ve suffered as a result of the defamation. For instance, you could show that your business has lost “x” amount of sales after the alleged defamation. For individuals, you could show you lost job opportunities, causing “x” amount of lost income.

When you sue someone for libel, the lawsuit is “actionable per se”. This means the court assumes that damage has been done to you. You don’t need to prove special damages.

With slander, the lawsuit is not actionable per se. The court does not assume damage has been done to you. You must prove special damages.

There are some important exceptions to this rule, however. The Defamation Act sets out some types of slander which are considered so harmful that special damages are assumed.

You don’t have to prove special damages for slander in the following categories:

Slander of women: Accusing or implying that a woman is unchaste or adulterous.

Slander affecting official, professional, or business reputation: Disparaging the professional reputation of someone, or the reputation of a business.

Slander of title: Slandering the quality of someone’s goods, or slandering someone’s right to a property.

If you’re a business owner, point 2 (slander affecting official, professional, or business reputation) is particularly important.

Not having to prove special damages makes it easier to file defamation lawsuits. It may not always be easy to show that your losses were directly connected to the alleged defamatory statement. For instance, if you run a business and lose several big contracts after the defamatory statements surface, it may be hard to prove that the statements were the primary cause. The court may decide that a multitude of other factors, like your business management, could have caused these losses – even if you know instinctively that it must be the defamatory statements harming your business.

Not having to show this greater burden of proof means you have greater ability to hold people who slander your business accountable for their words.

Can insurance protect against libel and slander?

Yes, absolutely! Professional Indemnity Insurance covers you from libel and slander lawsuits. If you accidentally make statements that end up defaming someone else, and they sue you for it, Professional Indemnity Insurance can protect you. This coverage would pay for lawyer’s fees, and damages/settlements stemming from the defamation suit against you.

Beyond libel and slander, Professional Indemnity Insurance also covers a broad range of other business lawsuits, including:

Negligence lawsuits

Errors & omissions lawsuits

IP infringement lawsuits

Patent infringement lawsuits

Joint venture liability

…and more

Click here to buy Professional Indemnity Insurance from $42/month, in 3 mins.

Protect your business with broad, affordable insurance

Make sure that you protect your business. We offer the most affordable and comprehensive business insurance plans in Singapore. Click the links below to get insured online, in just 3 mins!

Have you ever been told that “you can’t make a living as a writer”? That’s probably the biggest myth about freelance writing that exists in most people’s minds. Freelance writing is an excellent side gig for you to earn extra income while you hold a day job. Heck, if you’re really good at it, you could even quit your regular job and do content writing full-time.

Here’s a list of 11 of the most useful freelance writing tips that beginners need to know at the start of their creative journey.

#1. Start your own blog, preferably using WordPress

If you’re going to write for a living, it’s imperative that you have:

A platform for you to showcase your work and skills 24/7, and

A high-outreach, low-cost marketing channel for you to acquire new clients

A blog does both of the above things spectacularly well. So, which platform should you use? You should definitely start with WordPress. Why? With WordPress, you’re able to have full control over the look and feel of your site. You’ll be able to rank highly in search engines with SEO – much more so than with other sites like Medium. Once you’ve started your WordPress site, you can always syndicate your content to alternative sites like Medium and Tumblr. WordPress also allows you to be able to process payments, which you may want if you’re taking job bookings online.

Also, buy yourself a catchy domain name that’s easy to remember – GoDaddy has a great selection of these. Use a good hosting service, like Digital Ocean, that offers affordable and fast website hosting.

#2. Start contributing, even for free

There’s a million freelance writers out on the internet competing with you for the same writing jobs. The most important thing when you’re first starting out is to have a good portfolio of work that you can showcase to potential clients. Start writing lots of articles on your own blog to demonstrate your writing abilities. Then, start offering to contribute guest posts to other sites. These articles that you contribute could cover anything under the sun – it could be something that you’re knowledgeable about, something you’re interested in, or a writing niche that you think would pay well.

If you get paid for these articles – that’s all well and good. However, if you haven’t worked with the particular site before, or you don’t a list of previous clients you can talk about, you might not get offered any monetary compensation. That’s okay – if you’re just starting out. The credibility that you’ll be able to build with just a few articles published by someone other than yourself will be more important than the comparatively small, one-time fees you might get paid. And no, you’re not throwing yourself down some endless “do it for the exposure” rabbit hole – you’re just building a brand for yourself and getting a good head start in a very saturated, highly competitive field.

You’ll be much more likely to get signed on by clients if you can show them you’re not only capable of producing quality writing, but that other sites have trusted you enough to write for them.

#3. Network with other freelance writers

Even though freelance writing might seem like a solo adventure (and it often is), you can give your career a boost by forming great working relationships with other freelance writers just like yourself. You can ask more experienced writers questions about rates, handling clients, or even for project referrals. Having a professional network that you can tap on is never a bad thing, and you shouldn’t allow yourself to just operate in a silo as a freelance writer. Make the effort to actively connect with fellow professionals in your field, and you’ll find that it’ll pay off handsomely in the long run. Use a site like Meetup to connect with fellow freelance writers.

#4. Set aside time each day to read great content

Stephen King famously reads 80 books a year (that’s one-and-a-half books every week!). Why would one of the world’s most famous writers even bother with the writing of lesser mortals than himself? King says: “if you want to be a writer, you must do two things above all others: read a lot and write a lot.” The latter is almost guaranteed if you’re a freelance writer (doh!), but the first is certainly not. Many writers make the mistake of spending all their time producing, and not enough time absorbing. Yes, I get it – you don’t get paid to consume writing. But reading other people’s writing (and great writing, at that) is so essential to furthering your craft as a writer. How can you hope to deliver better writing each new day if you don’t learn from those better than you?

If a writer like King (who’s sold 350 million books) religiously reads writing other than his own, you definitely should too. Set aside at least an hour a day to read a diverse set of content, preferably from the top publications in each niche.

Here’s a useful set of reading material that writers would do well with:

News sites: Great learning for assignments that ask you to cover world events, politics, current affairs, or the like. You won’t go wrong with storied publications like The New York Times, The Guardian, or the South China Morning Post.

Magazines: Choose wisely here. Stay away from tabloids (unless that’s what you’re writing for). Editorials from Rolling Stone Magazine and Vox tend to be particularly eloquent.

Top fashion sites hardly need introducing: Vogue, GQ, and Womens Wear Daily are renowned staples.

Consumer product/service reviews: Lots of good choices here. Sites like PCWorld, Nerdwallet, or Wirecutter produce thoroughly researched, well-written content that’s read by millions of people.

By reading a diverse set of content, you’ll quickly become comfortable writing about any topic. The next time a job comes by on a topic you’ve never written about before, you’ll be twice as confident approaching it if you’ve been reading widely and religiously.

#5. Maintain the highest standards of professionalism

The freelance writing industry is filled with lots of cowboys who pump out shoddy work, oftentimes delivered with unethical practices like plagiarising other people’s content. Your reputation as a freelancer is everything, so make sure you are completely professional 100% of the time when dealing with clients. Here’s some useful professionalism tips for freelance writers:

Never plagiarise someone else’s work. Not only is this unethical, but you’re probably not going to achieve good results if you just copy-and-paste an existing article, and then make some minor edits. Search engines won’t rank the content well, and sharp-eyed readers/clients might even spot the similarities.

Use a professional email domain. Nothing gives a worse first impression than seeing a “gmail” or a “hotmail” address.

Answer emails/enquiries promptly.

Don’t undersell your abilities, but don’t oversell either – you want to manage expectations.

Don’t get upset at clients. If they’re demanding more revisions than necessary, or stressing you in some other way, state your position firmly but politely. A happy customer might tell a friend how good you are – an unhappy one will tell 10 about how bad you are!

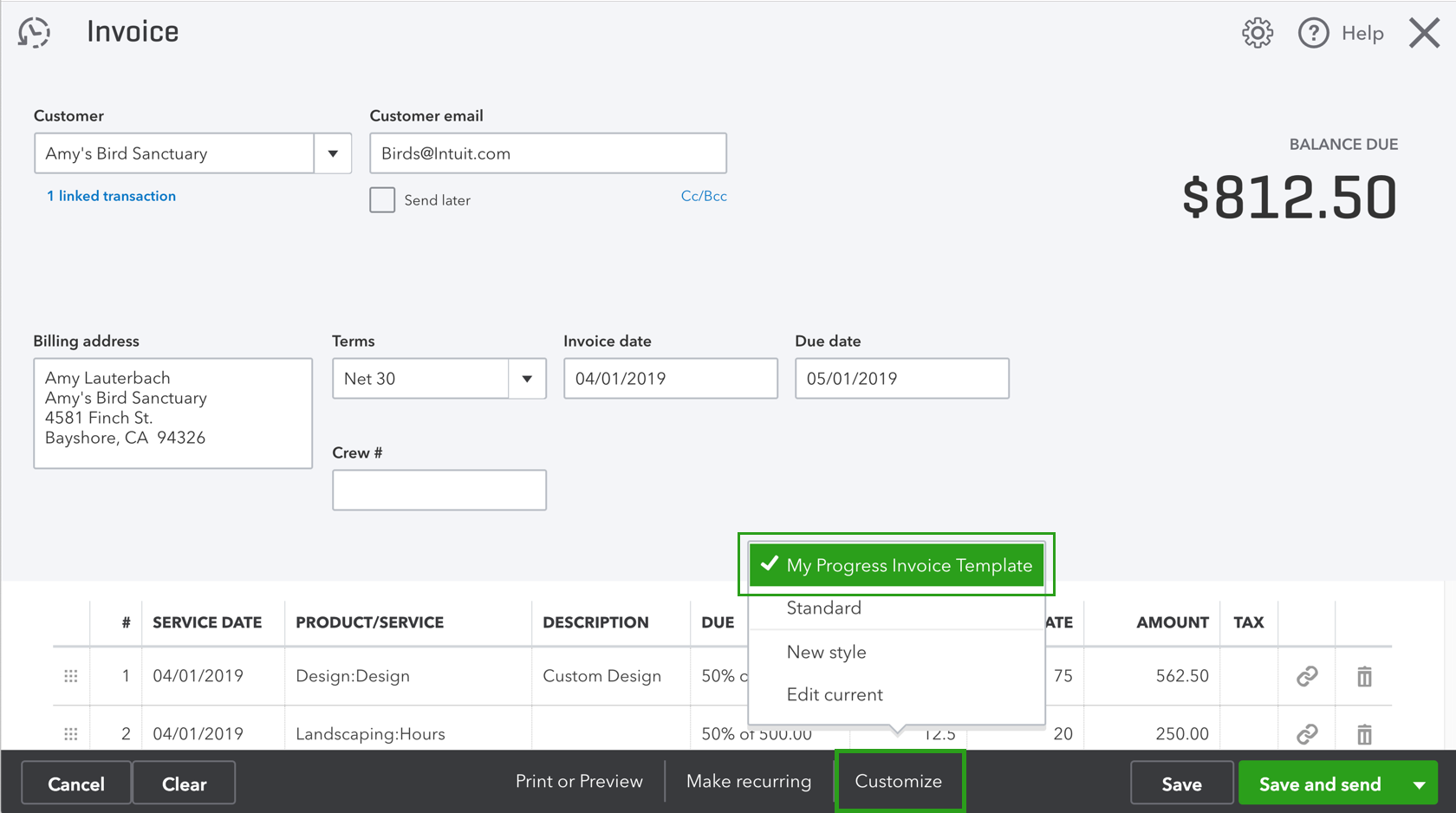

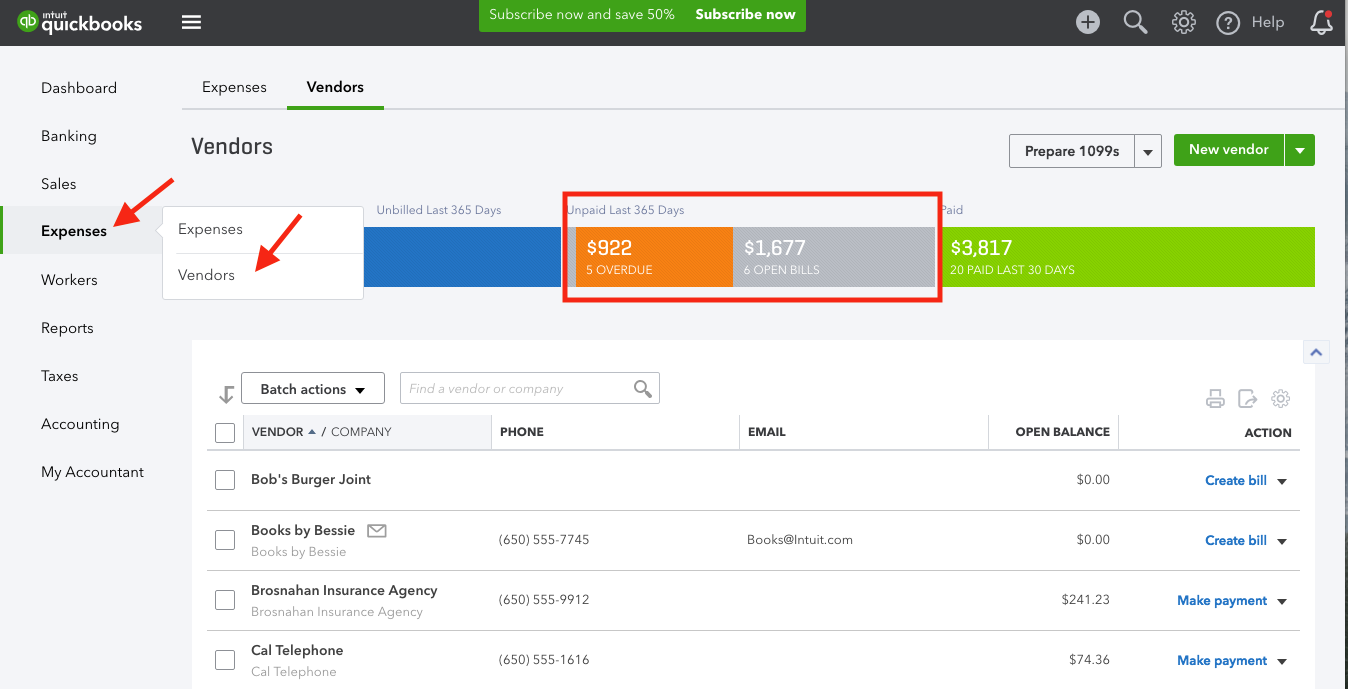

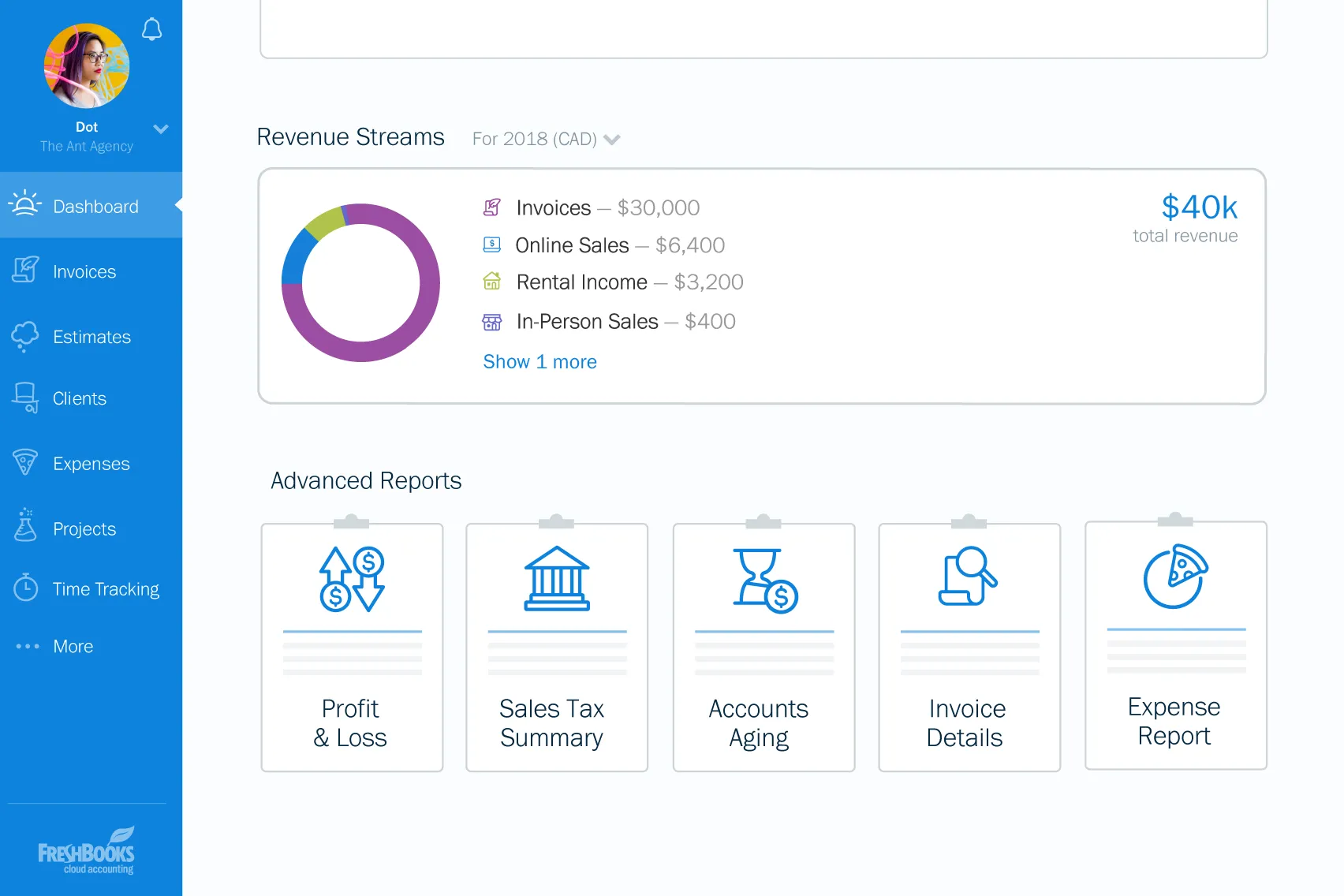

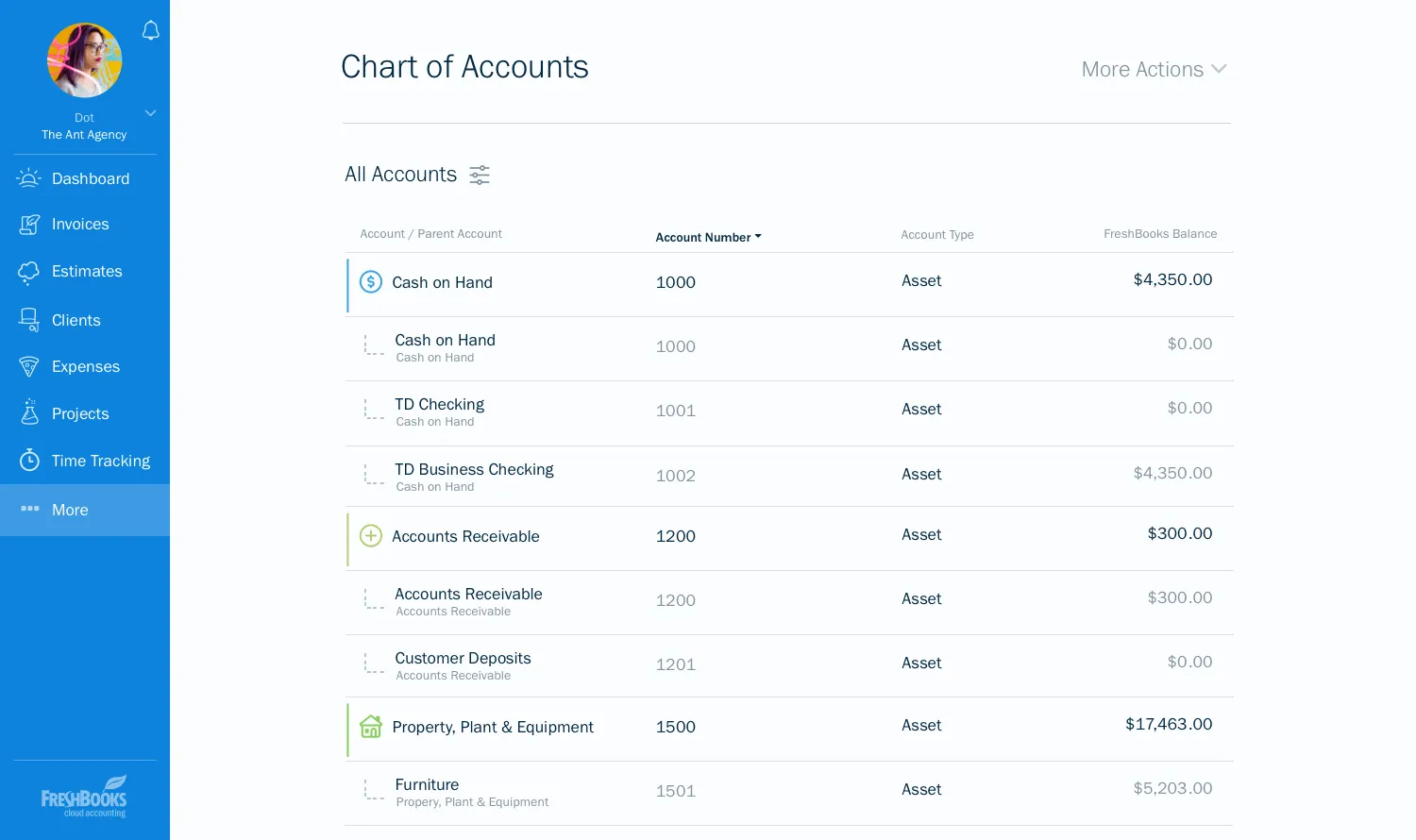

Send professional-looking invoices (check out our Xero review, FreshBooks review, and QuickBooks review, all of which give you great-looking invoice templates).

If you’re going to be late on a deadline, make sure you let your client know in advance. If something’s due at 11:59PM, don’t send an email at 11:50PM saying “Yeah, I’m gonna need 1 more day on that job you gave me”. If you’re really swamped, and you just need a little extra time, most clients will be understanding as long as you let them know early.

#6. Your qualifications are (mostly) irrelevant. The only thing that matters is your content.

Unless you have a specialized body of knowledge in a particular field, and your clients are looking to tap into that knowledge (e.g. you have a law degree and you’re writing law articles, or you know a particular industry in and out), your qualifications won’t mean anything. It’s really going to be irrelevant whether or not you have a university degree, or any other academic title – in freelance writing, those are (most of the time) just literally really expensive pieces of paper. So if you don’t have any of these qualifications, don’t feel like you’re less than. In this industry, the only thing clients care about is how good your writing is. The best way to move up the hierarchy of freelance writing is to write as much as you can, as best as you can, so that your writing skills and reputation become second to none.

#7. Develop a comprehensive marketing strategy

You’ll need to have a well thought-out strategy to market your services to clients. It’s not going to be enough to just dive in, thinking “I’ll just write for money”. There’s millions of other people offering the exact same service as you on the internet. How will YOU stand out?

The fundamental parts of a good marketing strategy for freelance writing are:

Search Engine Optimisation (SEO): You’ll definitely want to be on the first page of Google (and preferably in the top 3 positions) for keywords like “best freelancer writers for hire”, or “find freelance writer Singapore”. You’ll need to publish lots of great content for this (see tip 1), and ensure that your content is optimised for search engines.

Pay-Per-Click Ads (PPC) / Display Ads: This basically encompasses ads on Google AdWords, social media ads on sites like Facebook, and those banner display ads that you see on websites. You might want to consider buying ads to drive traffic to your business when you’re just starting out. Your website likely won’t be on the first page of Google yet for very many search terms, so ads will be the most effective way to get yourself customers.

#8. Get really good at keyword research

To be a great freelance writer, you’re going to want to get really good at keyword search. Your clients are probably going to judge the performance of your articles by how much readership they acquire. If your articles aren’t getting in front of people, they won’t be read, and you’re unlikely to get much repeat business from the same client.

Being skilled at keyword research allows you to hone in on the best choice of topics for your clients. If your client wants to write an article on a really competitive keyword, you can certainly take on the job. However, why not first suggest some less-competitive keywords for them to write content about? Having content pieces that rank on page 1 of Google is much better than having pieces that wallow in obscurity on page 10. (When was the last time you even clicked past Google’s first page?) This helps you add value to your clients, and also boosts your own content performance. If you perform smart keyword research, your articles are likely going to rank much higher in search engine results (SERPs). This is going to result in more views for your content, more brand awareness/sales for your clients, and therefore more repeat writing jobs for you. It’s a beautiful virtuous cycle.

Good tools for keyword research are SEMRush (USD 99/month) or Long Tail Pro (USD 37/month).

#9. Understand how your content fits into your clients’ overall marketing objectives

When you get a client who’s interested in hiring you to write something, make sure you understand their business, and what their broader marketing goals are. What is your client trying to achieve specifically with this content?

Some basic questions any good content marketer should be asking:

What are your content goals over the next 12 months?

How much revenue do you expect to generate from this content?

What is your targeted conversion rate?

How many leads do you want to generate?

What are your marketing objectives with this content?

Brand awareness

Lead generation

Conversions

Market education on products/services

Ask the right questions. Don’t just passively accept the writing assignment without understanding what the clients’ goals are. If you don’t try to understand your client’s goals, you’re not going to develop a deeper business relationship with them.

The most successful freelance content writers have a firm understanding of their client’s industry, what their client’s customers are looking for, and how to accomplish specific marketing goals via the content they’re publishing. These writers are the ones with the ability to charge the highest fees, the most loyal clients, and will earn the most repeat business. Remember, you’re not here to just churn out type. You’re here to intelligently analyse your client’s business/marketing needs, and then develop targeted pieces of content to address those needs. If you can do this, you’ll already be two steps ahead of the competition.

#10. Offer full-service content marketing

You’re probably not going to be able to charge very much if your only service is to passive take topics from clients, then churn out a bunch of words for them to use. You’re going to add much more value if you offer a full marketing service for your clients.

A full-stack content marketing service includes:

Formulation of marketing goals, and how content marketing fits into the overall marketing strategy

Keyword research

Topic generation/ideation

Writing

Follow-up analysis of performance, in relation to marketing goals

You can see that writing is really only one component (albeit the most important and time-consuming one) of the entire content marketing value chain. You’re going to create so much more value for your clients if you offer them services from steps A-E. Don’t just be a tool that clients use to pump out words – be the entire machine that creates ideas for them, relates the content to their business objectives, and then spins out beautiful content that helps them achieve their goals.

#11. You could start an agency, eventually

Freelance content writing is a great side gig that you can do to earn some extra income. But if you do this full-time, and do it really well, you could actually start your own content marketing agency. XXX is a great example of a content marketing agency, started by a couple that left full-time corporate jobs. They’ve just turned over $300,000 in annual revenue last year in this insightful blog post. Don’t underestimate the earning power of freelance writing. If you enjoy writing, you’ve probably been told by countless people that you “can’t make a living as a writer”. Well, actually you can. You’re probably not going to end up with millions of dollars and a private island to call your own, but you can definitely build a successful and fulfilling career out of writing.

Protect your freelancer business

Get liability insurance for your content writing agency.

Product Liability in Singapore: 6 Must-Knows for Small Businesses

Selling a defective product to customers can create massive liabilities for your business. If your items injure someone, don’t function as intended, or were even misleadingly advertised, you can be sued for product liability.

The median settlement cost of a product liability lawsuit is $1.5 million. Could your business handle such a huge expense? Product liability lawsuits are incredibly expensive, and could easily bankrupt most small businesses.

Here’s 6 things you have to know about product liability, and how to reduce your liability risk to protect your sales, your reputation, and your livelihood.

What factors lead to product liability lawsuits?

Your business can be held liable for product liability if the victim can prove:

Your product was defective

Your defective product caused injury

The product manufacturer, designer, or retailer owed a duty to provide the buyer with a safe product

It’s not only the consumer who directly buys your product who can hold you liable. Many third-parties can file lawsuits against you for product liability.

For instance, if someone gets injured in a bike accident because the bike’s brakes were faulty, they can sue the brake manufacturer for producing an item that didn’t work as it was supposed to.

In Singapore, your business can also be held liable for product liability by government regulators. This can occur if you use false/misleading advertising in your products.

#2. There are 3 types of defective products

A defective product is one that is not able to serve its original, intended purpose. Many products will have minor defects like cosmetic blemishes. However, the ones you should be concerned about are defects that could potentially cause harm to consumers.

The 3 main types of defects are:

Design defects: The product’s design makes it fundamentally flawed, causing danger to consumers even when they use it as instructed. A famous example is the Ford Pinto, a sub-compact car that was sold in the 1970s. The Ford Pinto had an inherently flawed design that placed the car’s fuel tank in a vulnerable position, causing it to be prone to explosions if hit from behind. This design caused a string of deadly fires to occupants. Ford was hit with 117 product liability lawsuits, and the company lost many millions in damage payments awarded to victims, plus many uncountable millions in lost sales due to their tarnished reputation.

Manufacturing defects: These occur when product manufacturers don’t follow the design blueprints correctly. These cause the product to become dangerous. In 2007, Mattel had to recall 967,000 toys in the US because their third-party manufacturer used lead paint to produce the toys. Lead paint is toxic, and has been linked to developmental issues in children who play with toys produced with such paint.

Marketing defects: These occur when insufficient/inaccurate/misleading information or instructions are provided with the product. In Singapore, the Consumer Protection (Fair Trading) Act allows customers to sue companies who use false claims to advertise their products. In 2017, AVA (Agri-Food and Veterinary Authority) took action against 4 margarine brands for falsely claiming their products had “zero trans-fat”.

#3. Adopt a proactive approach to reduce product liability risk

Perform detailed quality control and product testing before selling it to retailers or consumers

If you design and/or manufacture products, make sure you run your products through many rounds of rigorous testing to ensure that it doesn’t cause its users harm. This is the most important stage of limiting liability that could affect many people – potentially millions, depending on what you’re selling. Repeated tests will likely expose most of the defects in a product, allowing you to correct them before they end up in the hands of the public.

If you’re a retailer, make sure you research the products you’re stocking before actually putting them up for sale. Do research about the ingredients or the source of the product to ensure it’s not dangerous. You’ll also want to test your products to ensure they live up to their manufacturer’s claims. You can test your products in-house, or send them to an independent laboratory or testing agency to certify that they meet advertised standards, and are safe to use.

Have proper product information labels

Don’t include misleading claims on your product labels. Don’t leave out important or legally-required information from your labels.

If your product has a risk of causing injury to users, make sure you have a warning label and a set of instructions for proper use. The warning you give must be adequate to protect all foreseeable users of reasonably foreseeable dangers of the product.

You should be specific and transparent about potential risks that come with using your product. This way, if users end up getting injured or sick, you’ll be able to mount a stronger legal defence by stating that you effectively warned users about the risks that may come with using your product.

Inspect and maintain manufacturing equipment thoroughly

Maintenance might seem like a dreary cost, but it really is an important investment to ensuring that your goods come out consistent, well-built, and above all, safe. If you don’t maintain your equipment, it might not function properly, and may introduce serious defects into your products.

#4. Inform your broker immediately if you get sued for product liability

If you get hit with a product liability lawsuit, make sure you inform your insurance broker immediately. Your broker will then inform your insurer. Reporting this in a timely fashion is important, because your insurer could deny you coverage if you don’t.

You should also quickly seek advice from a good lawyer who specialises in product liability cases.

Your lawyer may, among other things, advise you to:

Gather documentation on all employees involved in manufacturing or selling the faulty product

Retain some samples of faulty products

Get employees and other relevant stakeholders to sign confidentiality agreements to protect any proprietary product knowledge

If you end up losing the product liability lawsuit, you’ll have to pay for legal expenses and damages. If you have product liability insurance, these costs will be covered for you by the insurance company.

#5. Take immediate action if you suspect product defects

Don’t wait until the defect results in someone getting hurt or sick. You need to act quickly before it’s too late. Defective products that end up harming your customers could cause irreparable damage to your reputation and your bottom line.

Here are some useful pre-emptive actions you can take to minimise your liability:

Issue a public statement that you’ve discovered a defect in your product.

Contact the distributors/retailers that sell your product, and inform them of the defect.

Communicate to consumers a specific plan to rectify the defect. You may have to offer refunds, discounts, or some other compensation to assuage public anger.

If the defect is serious enough, or could cause bodily harm, it’s best you issue a full product recall.

A case study of effective product liability management is how Toyota handled a fault in its hybrid vehicles. In 2014, Toyota issued a massive global recall of 2.4 million hybrid vehicles, after it discovered a defect that could cause the car to lose power. The recall was initiated before any accidents had actually occurred as a result of this power fault. As a result of Toyota’s swift and forward-thinking response, the carmaker avoided what could have amounted to tremendously destructive product liability lawsuits hitting it from around the globe.

#6. Protect your business from expensive product liability lawsuits

With the median product liability settlement costing $1.5 million, you’ll definitely want to have product liability insurance to protect your business. Small businesses could easily be bankrupted by such a massive cost.

Get yourself an online product liability insurance quote. You’ll get broad coverage, and save up to 25% on your premiums with Provide. Our online operating model creates lower overheads, so we pass every dollar saved back to you.

If your business manufactures products or sells goods, consider also investing in the following protection:

No business owner likes having the quality of their business questioned. However, there’s a difference between fair reviews and comments on a business, and attacks designed to harm the reputation of a company. If someone is spreading bad news about your products/services, talks bad about your company, or leaves scathing online reviews, you cansue them.

In Singapore, defamation against a business can be held to either be a criminal offence (Section 499 of the Penal Code), and/or a civil tort (Chapter 75 of the Defamation Act). There are 2 types of defamation: i) Libel, and ii) Slander.

Libel

Slander

Communication method

Permanent – written or broadcast

Temporal – spoken

Examples of communication mediums

Newspapers, articles, blog posts, social media posts, videos, radio broadcasts, TV shows

In-person communication, speeches, talks, comments at meetings

To sue someone for defaming your business, the statements in question must meet the 3 elements of defamation in Singapore.

Element #1. The statement must be defamatory in nature.

For a statement to be considered defamatory, the statement must meet 1 or more of the following criteria:

Lower the victim in the estimation of right-thinking members of society, or

Cause the victim to be shunned or avoided, or

Expose the victim to hatred, contempt or ridicule

For instance, a viciously opinionated online review would very likely fulfill the above standards. Such a review would cause your business to be held in lower regard (Criteria 1), and probably cause you to lose potential customers (Criteria 2). It might even invite people to make internet memes out of you, or mock your business on social media (Criteria 3).

Element #2. The statement must identify your business explicitly or implicitly

Explicit identification is simple: the defamer must identify your business or you directly. A review left on your Google page, a social media post titled “ABC Company Is Trash”, or videos that mention your business by name are all examples of direct identification.

However, identification can also be implicit. You can still sue someone even if they did not name your business directly, but made remarks or references that could be reasonably inferenced to identify your business. Examples of implicit identification include:

Making remarks about some aspect of your business that can be reasonably used to identify your company

Making remarks about a unique service or product that only you offer

Posting pictures of your products that can be reasonably linked to your business

Element #3. The statement must be communicated to a 3rd party

The defamatory statements must have been made known to someone other than yourself. For online reviews, or online comments, this standard is easy to meet, since the statements would have been published online and exposed to the public.

For verbal statements without written proof, or video/audio evidence, you can call upon witnesses to support your defamation claim.

Can I sue someone for writing a bad review about my business?

Yes, you can. The review must meet the 3 defamation elements as outlined above.

Can I sue someone for talking bad about my business?

Yes, you can. The review must meet the 3 defamation elements as outlined above. If the person is spreading rumours or criticism about your business without the use of published mediums that you can cite as evidence (e.g. he’s saying these remarks in-person to other people), you’ll have to call on witnesses to prove your case.

Defences against defamation

Defence #1. Justification

The defendant can win against your lawsuit by proving that the defamatory statement is true in substance and fact. For instance, say a client publishes this Facebook post about your business:

“ABC Company’s interior design services were so poor. The designs they gave us were so different from our requests, and they didn’t bother to include many details. They were also frequently late in submitting designs. Would not recommend at all.”

If you sued them, the client would have to prove the designs they received from you deviated significantly from their requests. They would also have to prove you didn’t meet submission deadlines. For instance, if they requested a French-style interior décor and you instead submitted a Japanese-style design, and you repeatedly sent designs days after you were supposed to, then they would prevail against your defamation suit.

Defence #2. Fair comment

The defendant can prevail against your defamation lawsuit by proving all of the following:

The statements in question were comments, not statements of fact.

The comments were based on facts.

The comment is fair, meaning it is something a fair-minded person would say or write. Some leeway is allowed for personal bias or exaggerations.

The comment is in the public interest, meaning it is something the public may be interested in knowing or have concern for.

In the case of a bad review, if the person you’re suing left a review that was composed entirely of opinions, then you are unlikely to win your defamation lawsuit against them. Take the following review for instance:

“The food tasted absolutely disgusting. The fish was so salty, the vegetables tasted bitter, and the meat was overcooked to death. I hope this place shuts down. Please do not EVER come here!!!”

Now, that’s a really nasty review. I’m sure if your business received a review like that, you’d be hopping mad. But are the contents of this review grounds to sue for defamation? The answer in this case, unfortunately, is likely to be no. The review doesn’t contain any statements of fact – in fact it’s composed entirely of opinions. That the food was “disgusting”, “so salty”, “bitter”, or “overcooked” are all matters of personal judgement, however strongly worded they might be (Criteria 1). These opinions were based on the fact that the reviewer dined at your restaurant, and did not personally enjoy the preparation of the food (Criteria 2). The statement can be adjudged to be reasonably fair (it did not contain a vicious litany of vulgar comments, for instance – Criteria 3). Also, it could be said that the statement merited public interest, since reviews help people to decide if a restaurant is worth visiting or not (Criteria 4). Because of these 4 defence elements, you likely won’t be able to successfully sue this angry reviewer.

Here’s another version of the above review, worded differently:

“The food tasted absolutely disgusting. Everything was terrible, and the restaurant was really filthy. I found dead insects in my soup. I even saw two rats running around on the floor! Please do not EVER come here unless you want to fall SICK!!!”

If you received a review like this, it would likely be grounds for you to sue for defamation. This review makes multiple allegations of fact. The poster claims the presence of harmful pests, insinuating there are serious hygiene lapses which could introduce diseases to patrons. Remember that when you sue for defamation, you don’t have to prove that the defamatory statement is false. Instead, the defendant must prove that their statement is true in substance and fact. In this case, the burden is on the defendant to prove that they in fact “found dead insects” floating in their soup dish, and in fact witnessed “two rats” scurrying around in your restaurant. If they can’t prove this to be true, then you’ll likely succeed in your lawsuit against them (hooray!).

In fact, you can not only sue for defamation in the above example – you could also sue the reviewer for spreading malicious falsehoods. If you can prove that the reviewer acted knowing that what they said was false, or they had intent to harm your business, you can seek further damages for the additional tort of perpetuating malicious falsehoods.

What compensation can you claim for defamation?

If you succeed in your defamation lawsuit, you can seek monetary damages. These damages are designed to compensate you for damage to reputation, damage to your business income, and to vindicate your name in public.

The amount of damages awarded will be based on:

The severity of the defamatory statement

How widely circulated was the defamatory statement

Any mitigating actions taken by the defendant (e.g. retracting the statement, issuing a public apology, etc.)

Sometimes, “aggravated damages” may be awarded in addition to regular damages (called “general damages”). Aggravated damages are compensation for the defendant’s behaviour or intent that cause additional harm to the plaintiff. For instance, if the defendant continues publishing more defamatory statements about you, even after being informed of the lawsuit/the untruthfulness of their statements, and they published especially malicious claims, that may be grounds for aggravated damages. Take note that Singapore’s High Court has ruled that aggravated damages can only be awarded for defamation against persons, but not corporate entities.

Suing for libel vs slander

If you sue for slander, you ordinarily have to prove that you suffered “special damages” – this is basically proving that you suffered quantifiable financial losses as a direct result of being slandered. Without proof of special damages, you won’t be able to sue. However, some exceptions to this rule exist: slander that affects official, professional, or business reputation does not require this proof. So, if someone slanders you as a company director, or your business, you don’t need to prove special damages.

If you sue for libel, you don’t have to prove special damages. The law automatically assumes you suffered special damages.

Just because you can, doesn’t mean you should

Launching a defamation suit against a hostile reviewer is much easier in Singapore than say, the US. The defence of fair comment is defined more narrowly here, unlike in America where the 1st Amendment covers all public opinions.

However, just because you can sue, doesn’t mean you should sue. From an operational perspective, launching a lawsuit against a single bad review is probably not the smartest thing to do. Why? Lawsuits are incredibly costly, and drain a lot of your time and energy. You could have spent the money on growing your business, and getting new customers who will actually leave your business positive reviews. Also, in this age of social media, the customer you’re suing could well expose your lawsuit against them online. The optics of a company suing an individual – potentially for something that others might deem trivial – are probably not going to reflect well on your business. By suing them, you might actually be shooting yourself in the foot by generating more bad press for yourself.

In 2018, a dessert shop in Singapore called Fantasy Desserts caused a big online commotion. The shop owner had publicly threatened to sue someone who had left a poor review of their food. The store owner engaged the reviewer with many combative remarks, and threatened to sue for defamation unless the reviewer deleted her unflattering opinion. Netizens swarmed to criticise the store owner, and the case even got picked up by news outlets like Asiaone and Mothership. The store closed in 2019. Whether or not the closure was due to the online furore is unclear, but it wouldn’t be difficult to draw a connection between its angry public threats, the permanent damage to its own reputation, and lost business. The amount of viral attention the store received (and not the good kind) is a clear lesson that good customer management, and not legal threats, should be your first response when handling public criticism.

Here’s a useful action plan for handling poor reviews or criticism of your business:

Respond politely, or just let the review/comments slide. There will always be that one unhappy customer out of all the clients you serve.

If the client continues to spread bad news about your business, or seems particularly upset, initiate a conversation directly with them. Why are they unhappy? Did they feel you didn’t deliver what you promised, causing them disappointment, disruption to their own affairs, or even financial losses? Try to work out a solution – maybe you could offer them a refund, a replacement, or try to rectify a mistake if you did make one.

If step 2 doesn’t work, and the client continues attacking your business, analyse how your business is being affected. If sales are noticeably being affected, then you should consider initiating legal action.

Ready to protect your business?

Online attacks against your company aren’t the only thing you should worry about. Employee injuries, business-related lawsuits, even getting sued for defamation yourself – these are all very real threats that your business will face everyday. Since we’re on the topic of defamation lawsuits, ask yourself this: what happens if a competitor accused you of defaming their business? Whether your competitors’ allegations are true or not doesn’t really matter, because you’d still have to hire a lawyer to defend yourself. And when it comes to hiring lawyers, let’s be real – it’s going to cost you a lot of money. Did you know that there’s a liability insurance policy that can protect you from such large legal costs? Enter Professional Indemnity Insurance.

Professional Indemnity Insurance covers the costs of defamation lawsuits. It pays for lawyer’s fees and the cost of damages/settlements. This ensures you’re not left with a large hole in your pocket. It also covers a wide range of other business-related lawsuits, like negligence lawsuits (e.g. you make accidental mistakes in your work, and a client sues you. That’s covered too.).

The cost of dealing with a massive lawsuit could bankrupt a small business. Don’t take any chances with your livelihood – make sure you protect your business with the best insurance policies possible.

Provide’s online platform helps business owners like you get quick & easy business insurance. Coverage is comprehensive, while premiums are affordable. Get these essential business covers now:

If you’re taking up professional indemnity insurance coverage, you’ve probably heard of the term “retroactive date” when arranging your policy. It’s a very important part of any liability insurance policy, so if your agent/broker didn’t walk you through what it means, maybe it’s time to switch to a better broker. (Hint: we’re really good at what we do.)

A retroactive date is the date from which your business has had uninterruptedprofessional indemnity insurance. From this date onwards, all liabilities you incur (subject to your policy’s wording, exclusions, etc.) will be covered by the insurer, no matter how far in the past they happened.

This means that if you’ve held continuous professional indemnity insurance coverage (with no lapses in coverage) from the day you started your business, you’ll be covered for all the years of services that you’ve provided in the past. So, even if you a lawsuit arises from work you did 10 years ago, you’ll be covered – as long as you didn’t have breaks in coverage!

If, however, there was a period of time when you did not hold professional indemnity insurance (for example, you cancelled your policy following the end of a contract or chose not to renew it), you will only be covered for work since the start of your new insurance policy.

What is the purpose of retroactive dates in professional indemnity insurance?

Retroactive dates are meant to exclude coverage for claims that arise before you bought professional indemnity insurance. They also function as a powerful incentive to keep your professional indemnity coverage continuous, because you’ll be covered for liability that might have occurred long ago but has only recently resurfaced to haunt you.

Retroactive dates are found in all professional indemnity insurance policies. This is because professional indemnity insurance is issued on a “claims made” basis (“claims made and reported” is the full technical term). This means that your policy will protect you from claims you make with your insurer while your policy is active, even if the event you’re claiming for events occurring before you bought your current policy.

What are the requirements to filing a claim under a “claims made” Professional Indemnity policy? There are 3 essential requirements:

You must have had coverage when the incident occurred

You must have coverage when you’re reporting the claim to the insurer

There can’t be lapses in coverage between the incident date and the reporting date

What are examples of how retroactive dates work?

Retroactive Date Example #1:

Let’s say you run a financial advisory firm. You provide M&A advice to a client. The deal closes and you move along, happy to have collected handsome fees. You had professional indemnity insurance during this period.

Right after the deal closed, you saw no need to continue paying for professional indemnity coverage. You allow the policy to lapse, and then buy a new professional indemnity policy later on.

However, several months after the deal closes, your client comes back to allege that you provided negligent advice on their deal. You file a claim with the insurer. Unfortunately, the insurer notifies you that you aren’t eligible for coverage, because you’ve had interruptions in your liability coverage. Your retroactive date is after the date of the incident you’re being sued for. Unfortunately in this case, you’ll have to pay for your own legal costs and damages – which are likely to be hundreds of thousands (or even millions) of dollars. If you had instead chosen to maintain your professional indemnity insurance, you would have been protected and the insurer would have stepped in to pay the costs for you.

Retroactive Date Example #2:

You run a construction company. In 2018, you finish a big project for a client. In 2022, this client discovers structural issues with the building. With the help of a building inspector, they determine it was your employees’ shoddy work that caused these structural instabilities. Your client sues you for negligence. You have held uninterrupted liability cover from 2018 to 2022.

When you file a claim with the insurer, you’ll be covered. Because you’ve held continuous liability cover, your retroactive date will be before the claimed incident. You won’t have to pay for legal costs out of your own pocket.

What are the different types of retroactive dates?

There are 2 main types of retroactive dates that you can request when purchasing professional indemnity insurance.

Type 1: Unlimited Retroactive Date

If your policy states that you have an unlimited retroactive date, it means that you will be covered for all work you’ve performed, regardless of how long it was done. You must still maintain active professional indemnity insurance to enjoy protection, but the insurer will not impose a time limit on the work that was done, even if it was a long time ago (e.g. 10 years ago).

Professional indemnity insurance policies with an unlimited retroactive date will cost more than policies with a specific retroactive date.

Type 2: Specific Retroactive Date (e.g. 1 January 2022)

If your policy contains a specific retroactive date, this means that liability for any work you performed before that date (e.g. 1 January 2022) will not be covered.

Specific retroactive dates are more commonly seen than unlimited retroactive dates.

How do retroactive dates work if I switch insurers?

Some insurers will provide you retroactive coverage even if you’re switching from another insurer, as long as you’ve held continuous coverage. However, other insurers will require that you’ve held continuous coverage with them only. This is completely dependent on the insurer you choose. If you’re shopping for a new professional indemnity policy, and you’re unsure which of these terms will apply, make sure to speak with an insurance broker – they’ll be the best person to assist you.

Send us an email at [email protected], or call us at +6588747011, if you are looking to switch Professional Indemnity insurers, and need advice on transferring your retroactive date.

How should I protect myself from liability for past work?

Easy: ensure your professional indemnity insurance is active at all times. Don’t let your cover lapse. Make sure you renew your policy. Although you might see it as an unnecessary expense, the amount you’ll pay for renewing your policy each year is much smaller compared to what you’d pay to defend a lawsuit. Many legal claims aren’t filed immediately against businesses – clients often don’t discover the negligence right there and then in the middle of busy projects. In fact, many claims against your business will happen several months, or even years, after the alleged negligent act occurred.

Always remember: Because retroactive dates function as a coverage cut-off point, dropping liability coverage for even one single day could cause you to lose all lawsuit protections if you get sued in the future. Without prior coverage for past work, you’ll be left completely exposed when your client’s lawyers come knocking at your door. You think you might be able to save a few thousand dollars, but you could very well instead be left with a legal bill for hundreds of thousands (or even millions of dollars). Professional liability is serious, and if you’re not careful could permanently damage the business you’ve worked so hard to build. Maintaining continuous coverage is something business owners must take very seriously!

How long should I keep professional indemnity insurance active if my business is no longer around?

It really depends on what kind of business you used to run.

Businesses that are exposed to large amounts of potential liability, like construction-related businesses, may need to keep professional indemnity insurance active for many years (e.g. 5 years or more) even after they stop operating their company. This is because structural defects that can result in lawsuits commonly occur only years after the project is completed. An architect or construction contractor could complete a project successfully, but get sued only 5 years later when defects in the building start showing up.

In general, a rough rule-of-thumb would be to keep your professional indemnity insurance active for at least 3 years after you’re no longer running your business. A minimum of 3 years strikes a balance between maintaining protection and maintaining a reasonable amount of insurance expenditure. If you understand the severity of legal costs enough to purchase professional indemnity insurance in the first place, then ensuring you renew your policy even after your business closes should be a natural thing to do. The last thing you want is to close your business, retire into the sunset (or start another business), and then find legal papers being served onto you without having any insurance protection!

Where can I get great professional indemnity insurance?

You can buy Professional Indemnity Insurance on our website, within 3 minutes. Simply fill in the details below, and you can get your policy in a few clicks.

What’s the difference between Public Liability and Professional Indemnity?

Public liability is used to protect businesses from third-party lawsuits due to injury or property damage caused by your business operations. Professional Indemnity is used to protect businesses from client lawsuits due to services they’ve provided.

Public Liability vs Professional indemnity Coverage

Coverage

Public Liability Insurance

Professional Indemnity Insurance

Physical injury or property damage to third-parties (e.g. customers, members of the public)

Yes

No

Professional errors & omissions

No

Yes

Defamation

No

Yes

Here are real-world public liability vs professional indemnity claims examples, which will illustrate the differences in more detail:

Example Company

Public liability

Professional indemnity

Construction firm

You’re constructing a building, and accidentally damage surrounding properties.

You’re liable to the property owners for the damage you caused them due to your business operations.

You’re constructing a building, and your workers do a shoddy job causing structural instability.

You’re liable to your client for financial losses you caused them due to your negligence/errors/omissions.

Doctor’s clinic

A patient slips and falls in your clinic, injuring themselves.

You’re liable to the patient for their injury, since it was caused by your business operations.

Your medical advice worsens the patient’s condition.

You’re liable to the patient for causing them bodily harm due to your negligence/errors/omissions.

Financial services firm

You post some advertising signboards in public. One of your signboard falls on a pedestrian,injuringthem.

You’re liable to the pedestrian for their injury, since it was caused by your business operations.

You trash a competitor with exaggerated claims about how bad their business is.

You’re liable to the competitor for defamation.

In each of the above scenarios, this is how each type of insurance would respond to protect your business against legal liability:

PublicLiability Insurance: This policy would protect you from the legal fees and damages awarded to your injured client. Some public liability policies will also have Food & Beverage extensions, which will cover food poisoning caused by your business.

Professional Indemnity Insurance: This policy would protect you from the legal fees and damages awarded to your client.

Common misconceptions about public liability vs professional indemnity:

#1. Public liability covers liability to the entire “public” body right? So shouldn’t it cover me if I make mistakes while providing a service to clients?

Nope. Public liability is designed to protect you when your business accidentally causes injury or damage when conducting business activities in public, or that involve congregations of people. It’s not designed to protect you if you make a negligent mistake while providing your services. In fact, public liability policies will often come with clauses that will expressly exclude coverage for any protection offered by a professional indemnity policy.

#2. Public liability should cover me if my business makes defamatory statements, right?.

That’s another nope. Public liability will not protect you if you make defamatory statements about someone else, like a competitor. Defamation encompasses slander (which is spoken), and libel (which is written). Only professional indemnity would cover you if you had committed such an act.

Do businesses need both public liability and professional indemnity insurance?

If your business involves providing any kind of services to clients, then yes – you need both insurance types. As you’ve seen in the above examples, public liability and professional indemnity protect you from very different – and very real – risks. If you only have one or the other, then you’re really exposing yourself to 50% more risk. If you have one of these policies, make sure to get the other so that you’ll be fully protected against lawsuits.

If your business sells only goods instead of services, then instead of professional indemnity, you’ll need a product liability policy. Product liability insurance will protect you from lawsuits targeting your business because of injuries or damage caused by goods you sold. Depending on what kind of goods you sell, the potential liabilities on your business may be huge. For instance, if you sell car parts to auto workshops that later turn out to be defective, you could cause fatal car accidents. You’d be legally liable for someone’s death in that scenario.

How much does it cost to have both public liability and professional indemnity insurance?

Public liability insurance is very affordable, with a large amount of $1,000,000 coverage starting at only $16/month (depending on the industry). That’s the price of a single meal in a restaurant!

Professional indemnity insurance will have higher premiums, and due to its highly tailored nature, quotes can only be produced with more precise information about the business seeking coverage. Get in touch with us for a quote on professional indemnity coverage for your company.

Remember that with Provide, you save up to 25% on your insurance premiums. Thanks to our digital operating model, our overheads are much lower, and we pass every dollar saved back to our clients.

Sometimes business owners might brush off the need for commercial insurance, viewing it as an unnecessary expense for a risk that will never materialise. We would urge extreme caution in this regard – legal liability is one of the most serious risks any business can face, particularly for small businesses that have limited resources to handle sudden, large expenses.

What are the typical coverage amounts businesses should have

What other types of liability insurance do businesses need?

In addition to public liability and professional indemnity, businesses should also have:

Directors & Officers (D&O) Liability Insurance: This type of insurance protects company directors & officers from personal legal liability. Most company directors are blissfully unaware that their position exposes them to a stunningly wide variety of legal liabilities. Get an instant D&O insurance quote here.

WICA Insurance (Work Injury Compensation): This type of insurance protects the business from liability when workers get injured on the job. Under the 2012 WICA Act, your workers can file a WICA claim against you if they get hurt or sick due to work-related causes. You’ll have to pay their medical fees and damages if the WICA claim is approved by the courts. MOM (Ministry of Manpower) regulations also stipulate mandatory WICA insurance for employees earning less than $1,600/month, or employees performing manual labour. Get an instant WICA insurance quote here.

Where can I get great public liability and professional indemnity insurance quotes?

Get broad-coverage and affordable quotes for public liability here, and professional indemnity here. With Provide, you save up to 25% on your insurance premiums. Our digital operating model creates lower overheads, and we pass every dollar saved back to you.

Xero Review 2020: Online Accounting for Small Business

Pros

Cons

Rich accounting features

User interface could be more intuitive

UI fairly intuitive

Customer support takes longer than needed to respond, needs improvement

Can generate 80+ different accounting reports